Aggregate Supply

According to traditional economists, full employment determines the level of national income. To clarify the theory of income and employment, JM Keynes created the idea of effective demand. At full employment or a level below full employment, a country can achieve balance. Effective demand is mainly determined by two factors, aggregates of both supply and demand. Aggregate demand is the demand for products and services across the whole economy, and it includes all consumer spending on both commodities and services.

The total amount of goods and services generated in an economy over a specific period is referred to as aggregate supply. In other words, it is the total amount of final output that is made accessible to the economy for purchase at any particular time. The cost incurred by the plant to manufacture the final goods and services is equivalent to the value of the excellent final output, and producers are required to recoup these costs through the sales they generate.

Supply overall is equal to consumption plus savings.

Traditional Supply of Aggregates

According to classical economics, real wages adapt quickly to provide full employment at all times, and wages and prices are totally flexible over the long term.

Thus, the supply of aggregate over the long term is vertical. Long-term unemployment is impossible because all employees who want a job will be given one, regardless of the price level, and output will always remain constant at the income level required for full employment. A change in aggregate demand has an impact on output and employment but is completely powerless. The price level is entirely responsible for changes in aggregate demand. Equilibrium shifts higher with the Aggregate demand moving to the right. Real output is unchanged, however, prices are increasing. According to traditional economists, AS is vertical in the long run.

Aggregate Supply Under Keynesianism

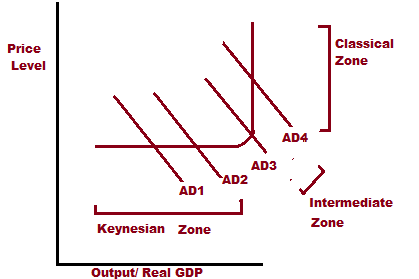

The aggregate supply curve shows three ranges. Keynesian, classical, and intermediate. The economy is operating at traditional full employment. The aggregate supply is the total amount of goods and services that the nation's businesses plan to sell during a specific period. It is the total amount of goods and services that companies in an economy are able and willing to offer for sale at a certain price point.

A rise in Aggregate demand results in an increase in real output with no change in price in the Keynesian zone (horizontal segment), an increase in output with no change in price in the intermediate zone, and an increase in output with no change in price in the classical zone.

Aggregate Supply (AS) is the money worth of all final goods and services available for purchase by an economy over a certain period. It is the economy’s movement of goods and services. AS equals national income because the monetary worth of final goods and services equals the net value-added. The country’s national revenue is represented by aggregate supply. Y = AS (National Income).