Elasticity: What Is It?

Let's say rubber and bricks. What is more resilient? Of course, you say rubber is more resilient than brick. Applying force to it increases the length of the rubber. There are two variables here. One is power and the other is (length) quantity. Economics also uses price as a force that checks the elasticity of quantity demand and supply.

In economics, elasticity measures the responsiveness of demand to changes in price. It is a key concept in business and economics because businesses produce goods and services to meet the demands of consumers. Consumers’ demand for goods and services is elastic when they are responsive to price changes. In other words, they purchase more when prices decrease and buy fewer when prices increase. Therefore, elasticity can be used as a tool to understand consumers’ reactions to pricing strategies

Both income and price influence consumer behavior; therefore, both types of elasticity should be considered when analyzing consumer data. Income elasticity refers to how an increase in income affects consumer demands for goods and services; price elasticity refers to how price decreases affect purchases. A positive price elasticity indicates that as prices decrease — either through government intervention or market forces— consumers will purchase more goods and services. On the other hand, a negative price elasticity indicates that as prices increase— either through market forces or charity — consumers will purchase fewer goods and services than before at higher prices.

Elasticity can be visualized graphically by the appearance of the supply or demand curve.

A fully elastic curve will be level at the extremes and a perfectly inelastic curve.

A more elastic will be horizontal, and a less elastic will be vertical.

Types of Elasticity of demand

Price Elasticity of demand

Income Elasticity of demand

Cross elasticity of demand

Price elasticity of demand

It refers to the percentage change in quality demand due to a certain percentage change in price, other conditions being equal. Mathematically, it is described as follows:

𝐸𝑝=(𝑃% change in demand)/(% change in price)

𝐸_𝑃 = (Δ𝑄/𝑄×100)/(Δ𝑝/𝑃×100)

where ΔQ = change in quantity demanded ΔP = change in commodity price P = initial price Q = initial quantity demanded.

Numerical: Calculate the price elasticity of demand from the given table.

|

price quantity

|

Quantity demanded

|

|

10(P1)

|

5(Q1)

|

|

20(P2)

|

2 (Q2)

|

Solution.

Del P = P2 – P1 = 20 – 10 = 10

Del Q = Q2 – Q1= 2 – 5 = -3

Ep = -3/5/10/10

Ep = - 0.6

The negative sign indicates price and quantity demanded are inversely related. It means a 1% increase in price equals a 0.6% decrease in demand.

Degrees of price elasticity of demand

Perfectly elastic demand(Ep= infinity)

Perfectly inelastic demand(Ep=0)

Unitary elastic demand (Ep=1)

Relatively elastic demand(Ep >1)

Relatively inelastic demand(Ep <1)

Perfectly elastic demand(Ep= infinity)

Demand is said to be perfectly elastic if a very small change in the price of a good causes an infinite change in the quantity demanded of that good.

In the diagram below, OP is the price of quantity Q1. There is a negligible price change when demand increases from Q1 to Q2. This shows infinite variation.

This is a fictitious situation and not seen in the real market.

Perfectly inelastic demand

If there is no change in quantity demand due to a certain percentage change in price is called perfectly inelastic demand.

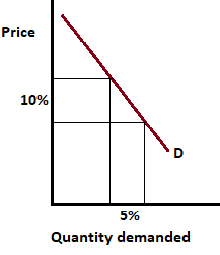

Relatively elastic demand

If the percentage change in quantity demand is greater than the percentage change in price is known as relatively elastic demand. For example 10% change in demand due to a 5% change in price.

Relatively inelastic demand

If the percentage change in quality demand is a percentage change in price is known as relatively inelastic demand. For example 5% change in quantity demand due to a 10% change in price.

Unitary elastic demand

If a percentage change in the price commodity is equal to the percentage change in quantity demand then it is known as unitary elastic demand.

Ep = % change in quantity demanded/% change in price

= 10%/10%

= 1

Income Elasticity of Demand

It refers to the percentage change in quantity demand due to the certain percentage change in income of consumers when other things remain the same.

Mathematically,

𝐸𝑦=(Δ𝑄/𝑄)/(Δ𝑦/𝑦)

Degrees of Income Elasticity of Demand

Positive income elasticity of demand(Ey>1, Ey<1, Ey = 1)

Zero Income Elasticity ( Ey = 0)

Negative Income Elasticity of Demand(Ey<0)

Positive income elasticity of demand greater than one(Ey>1)

If the percentage change in quantity demand is greater than the percentage change in income is known as income elasticity of demand greater than one.

For example, a change in demand by 10% due to a change in income by 5%.

Ey = % change in quantity demanded/% change in income

= 10%/5%

= 2 > 1

Income elasticity of demand less than one

If the percentage change in quantity demand is less than the percentage change in income is known as income elasticity of demand less than one.

For example, a change in demand by 5% due to a change in income by 10%.

Ey = % change in quantity demanded/% change in income

= 5%/10%

= 0.5<1

Income elasticity of demand equal to one(Ey = 1)

If the percentage change in quantity demand is equal to the percentage change in income is known as income elasticity of demand equal to one.

Ey = % change in quantity demanded/% change in income

= 10%/10%

= 1

Zero Income Elasticity of Demand

If there is no change in the quantity of demand due to a certain percentage change in income then it is known as zero income elasticity of demand.

Ey = % change in quantity demanded/% change in income

= 0%/10%

= 0

Negative Income Elasticity of Demand(Ey<0)

If there is a negative relationship between income and demand in this case income elasticity is negative. In this case, inferior goods' income elasticity is negative.

Ey = % change in quantity demanded/% change in income

= 5/-10

= -0.5

Cross Elasticity of Demand

It refers to the percentage change in quantity demand of one commodity i.e. x due to a certain change in the price of another commodity i.e. y when other things remain the same.

The measure of the responsiveness of quantity demanded goods x to the change in the price of goods y is known as cross elasticity of demand.

Mathematically,

Exy = Percentage change in quantity demanded goods x/ Percentage change in the price of goods y.

Exy =(Δ𝑄𝑥/𝑄𝑥)/(Δ_𝑃𝛾/𝑃𝑦)

Degrees of Cross Elasticity of Demand

Positive cross elasticity of demand:(Exy>0)

Zero cross elasticity of demand(Exy =0)

Negative elasticity of demand(Exy< 0)

Positive cross elasticity of demand(substitute goods):(Exy>0)

Cross elasticity of demand is positive because when the price of product X increases, the demand for product Y also increases.

Substitute goods will have a positive cross-elasticity of demand.

Complements will have a negative cross-elasticity of demand

Cross elasticity of demand is 0 for unrelated goods because consumers will continue to buy product x even if the price of product y rises.

Cross-elasticity of demand for unrelated commodities will be zero.

Negative demand elasticity (Exy 0)

Cross elasticity of demand for complementary items is negative because as the price of good A falls, so does the demand for good B, and vice versa.

The demand for a computer is not affected by an increase in the price of oranges.

Elasticity

of Supply

Price

elasticity of supply calculates the relationship between change in price and

change in supply.

Es=Percentage change in supply/Percentage change in price

Es=(ΔQ/Q×100)/(Δp/P×100)

Degrees of price elasticity of Supply

Perfectly elastic Supply (Es= infinity)

Perfectly inelastic Supply(Es=0)

Unitary elastic Supply (Es=1)

Relatively elastic Supply(Es >1)

Relatively inelastic Supply(Es <1)

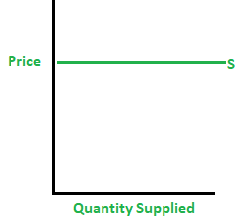

Perfectly elastic supply(Es= Infinity)

If a very small change in the price of goods leads to an infinite change in the quantity supplied for that goods, then the supply is known as a perfectly elastic supply. Graphically,

Perfectly inelastic Supply (Es= 0)

If there is no change in quantity supplied due to a certain percentage change in price is called perfectly inelastic supply. Graphically,

Unitary elastic Supply(Es = 1)

If the percentage change in the price of a commodity is equal to the percentage change in quantity supplied then it is known as unitary elastic supply.

Graphically,

Relatively elastic Supply(Es >1)

If the percentage change in quantity supplied is greater than the percentage change in price is known as a relatively elastic supply. For example, a 10% change in quantity supplied due to a 5% change in price. Graphically,

Relatively inelastic Supply (Es<1)

If the percentage change in quality supplied is a percentage change in price is known as a relatively inelastic supply. For example 5% change in quantity supply due to a 10% change in price.

Determinants of price elasticity of demand

The elasticity of demand depends on the availability of substitute goods. When a commodity has many substitutes, the elasticity of demand decreases. For example, apples are more elastic than salt, because apples can be replaced with oranges.

Demand for necessary commodities such as salt, rice, and vegetables is inelastic as changes in the price of commodities have little effect on the quality of the demanded commodities. Demand for luxury goods such as sofas, cars, and ornaments is very elastic. Because they contribute to the comfort of life and people can live without them, a small price change will result in a large change in the quantity demanded.

Power demand is highly elastic due to multiple uses. Lower electricity prices will allow consumers to use electricity for multiple purposes, such as cooking, washing clothes, and ironing. In this situation, the power demand increases significantly.

The elasticity of demand also depends on the income levels of consumers who have diverse (abundant) sources of income and are insensitive to small price fluctuations of goods and services. Therefore, the demand for goods is inelastic. Poor consumers are very sensitive to small changes in commodity prices.

Some commodities, such as wine, tobacco, and medicine, are known as necessities. Consumers accustomed to these goods do not react to small changes in price. The quantity demanded of such goods remains inelastic to changes in price levels.

There are other factors also such as time factor, consumption shift, and price level which also affect the elasticity of demand.