Equilibrium analysis

The equilibrium analysis is important and plays a prominent part in economic theory.

Equilibrium implies all states of balance or a state of rest. when two opposite forces balance each other on a particular subject then that object is in equilibrium.

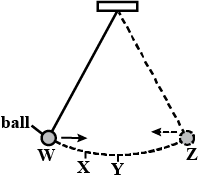

let's illustrate if we tie a stone with a string and hang it from a nail fixed in the wall, it oscillates more to and fro and after some time it comes to stand in the center if no further disturbance is caused to it. The central point where the string finally comes to rest is the equilibrium point. at that point, the two opposite forces are exactly equal and balanced against each other And there is no more movement to be found in the string.

In economics, equilibrium does not necessarily mean an absence of a moment. in fact, the economic system would collapse if all movements in it come to a standstill. the idea is not that the moment should cease, the idea is that there should be no change in the rate of the moment for example the production and consumption rate should not change in an economic system.

An individual consumer is in equilibrium when someone enjoys maximum satisfaction from a given spend on different goods and services. once someone reaches an equilibrium position, s/he sticks to it because any change in the allocation of income between two different goods and services will reduce his total satisfaction. likewise, the form is in equilibrium when it maximizes its profit or minimizes loss in a given situation.

The firm too will have no incentive to deviate from the equilibrium position. In a similar manner industries are said to be in equilibrium there is no tenancy for the size of the industry to change that is, when no forms with to leave it and no new forms are being attracted to it, the marginal in the industry just making normal profit neither more nor less.

In short, the essence of an equilibrium position is that no participant believes someone can improve the slot by altering his behavior. According to professor building if you know where the train is going then know it is at any moment.

The supply curve is trending upward in this graph while the demand curve is sloping downward. The red part represents a surplus, whereas the yellow part is a shortage. The point with a green tint represents the point of equilibrium where demand and supply from the market interact and reach a stable state.

Types of Equilibrium

- Stable Equilibrium

- Unstable equilibrium

- Neutral Equilibrium

Partial Equilibrium

Partial equilibrium is the process of developing a model with only two variables, known as the independent variable and the dependent variable. The dependent variable will be impacted by the independent variable, which is what you want to change.

It is a particular kind of equilibrium where the market's quantity and price are not entirely predetermined. This is because a variety of factors, such as the following, have an impact on market price and quantity:

Consumer preferences, income levels, and other factors influence demand for products and services. The availability of goods and services is based on the cost of production, the cost of labor, and other factors. Government policies can have an impact on the supply-side or demand-side of an economy (e.g., subsidies). The market pricing and volumes can also be influenced by other external factors, such as the weather.

General Equilibrium

An economy is said to be in general equilibrium when all markets operate at their highest efficiency levels. When all markets are in balance, an economy is said to be in general equilibrium.

According to the concept of general equilibrium, supply and demand alone determine prices and quantity, with no outside influences. When this occurs, it indicates that no room exists for any economic activity to advance toward the ideal point. Although it may be argued that this is a very ideal circumstance, it does not occur in the real world.

Adam Smith introduced the idea of general equilibrium in his book "Wealth of Nations." He thought that if the government did not interfere and each market was allowed to operate on its own, there would be no economic issues. As economies have changed and grown more complicated, this idea has been disproven throughout time. According to economists today, a stable economy needs some kind of government involvement to keep it operating at its best levels (i.e., full employment).